An In-Depth Comparison of Cheese and Self to Help You Make an Informed Decision

Establishing and improving your credit score is essential for long-term financial success. Cheese Credit Builder and Self Credit Builder are services designed to help individuals with no or poor credit establish a solid credit history. In this comprehensive comparison – Cheese vs Self- we will examine both services’ features, benefits, and costs, empowering you to make the best decision for your credit-building journey. Our analysis will include an overview of each service, comparing their features and benefits, customer reviews, and similar offers in the market.

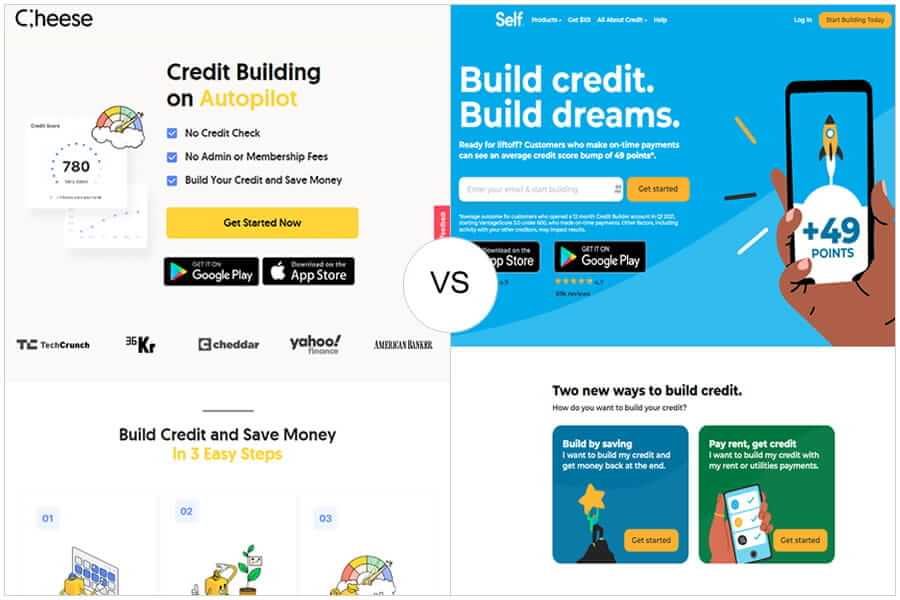

- Discover Cheese – A credit builder service that helps users establish and improve their credit scores through flexible repayment plans, potentially lower costs, and faster credit reporting timelines while offering an FDIC-insured savings account.

- Discover Self – A credit builder service that assists users in building their credit scores by offering fixed 24-month plans with an FDIC-insured savings account, reporting payments to the three major credit bureaus, and charging a one-time $9 admin fee.

Overview of Cheese Credit Builder

Cheese Credit Builder, a California-based Cheese Financial Inc. service, is dedicated to helping users build credit and grow savings through simple and automated solutions. Cheese offers a credit builder loan that allows customers to make monthly on-time payments, which are reported to all three major credit bureaus (TransUnion, Equifax, and Experian) and added to their credit builder account. Partnering with Lineage Bank, an FDIC member, Cheese ensures customer deposits are FDIC-insured.

Unlike many competitors, Cheese does not charge upfront or admin fees. The only cost is an APR ranging from 5% to 16%, depending on the customer’s state of residency. Cheese Credit Builder boasts six flexible loan plans, providing options suitable for various budgets and needs. Customers can diversify their credit mix by adding a personal loan to their credit profile, which may help improve their credit score.

Overview of Self Credit Builder

Self Credit Builder Account, formerly Self Lender, is a fintech platform based in Austin, TX, that offers credit-builder loans and a self-secured credit card. The platform allows consumers to simultaneously build savings and credit by reporting payments to all three major credit bureaus. This reporting helps establish a credit history for those with little to no credit.

Self offers four payment options to accommodate varying budgets. There is a nonrefundable administrative fee of $9 and an APR of 15.65% to 15.97%. Upon signing up, Self deposits the loan proceeds into a certificate of deposit (CD) and holds them until the program is completed. During the payment term, customers’ payment activity is reported to the credit bureaus, helping to build their credit score. At the end of the payment term, Self returns the customer’s monthly payments minus any applicable interest and fees.

Cheese vs Self Comparison Table

In this section, we will compare the key features and benefits of Cheese and Self in detail, highlighting their similarities and differences. Both services are credit builder loans that report payment history to the three major credit bureaus, helping users establish credit. After the loan matures, customers receive the paid principal back minus the interest.

| Features | Cheese Credit Builder | Self Credit Builder |

|---|---|---|

| Company | Extra Financial, Inc | Self Financial, Inc. |

| BBB Accredited | Cheese | Self |

| Type of Entity | Corporation | Corporation |

| Headquarters | 130 W Union St, Pasadena, CA 91103-3628 | 901 E 6th St Ste 400, Austin, TX 78702-3206 |

| Social Media | ||

| Business Started | Not disclosed | 6/1/2014 |

| Loan Terms | 12 and 24 months | 24 months |

| Loan Amounts | $500, $1,000, and $2,000 | $520, $724, $992, and $3,076 |

| Monthly Payments | $23.54 – $177.701 | $25 – $150 |

| APR | 5% to 16% (varies by state) | 15.65% to 15.97% |

| Upfront/Admin Fees | None | None |

| Credit Reporting Timelines | 10-30 days2 | BBB Accredited |

| Credit Check | No (Soft Pull) | No (Soft Pull) |

| FDIC Insured Deposits | Yes | Yes |

| Credit Reporting Bureaus | TransUnion, Equifax, Experian | TransUnion, Equifax, Experian |

| Account Holding Institution | Lineage Bank | Self (Certificate of Deposit) |

| Early Loan Repayment | Allowed | Allowed |

| Customer Support | BBB Accredited | Email, phone, and help center |

| Phone Number | (866) 657-8863 | (877) 883-0999 |

| Years in Business | Not disclosed | 8 Years |

| BBB Rating | N/A | B |

| BBB Acredited | No | Yes, since 1/27/2016 |

| Mobile App | Yes | Yes |

| Google Play | 50K+ downloads | 1M+ downloads |

| Apple Store | N/A | N/A |

| Claim this offer | Claim this offer |

Please note that the exact details of the features, pricing, and ratings may vary and should be verified with the respective services before making any decisions. The information provided here serves as a general overview and comparison between Cheese Credit Builder and Self Credit Builder.

Cheese vs. Self Similarities

- Credit Reporting: Cheese and Self prioritize helping customers build their credit scores. They achieve this by reporting your payment history to the three major credit bureaus – TransUnion, Equifax, and Experian – ensuring your responsible repayment habits are reflected in your credit report. (See: Credit Cards Reporting Credit Explained)

- Safety: Deposits made with both Cheese and Self are FDIC-insured, offering customers peace of mind regarding the safety and security of their funds. This means that even if the financial institutions behind these services were to fail, customers’ deposits would still be protected up to the FDIC insurance limits.

- Function: Cheese and Self share the goal of helping customers build their credit scores and save money simultaneously. They both offer credit builder loans or secured loans that, when repaid responsibly, can significantly improve a customer’s credit rating over time.

Cheese vs. Self Differences

- Loan Plans: Cheese offers greater flexibility in repayment options, featuring six plans catering to various budgets and financial goals. Self, in contrast, only provides four plans, all with a fixed 24-month duration. This means Cheese might be a better option for customers looking for more tailored loan plans that suit their unique needs.

- Costs: Cheese has a clear advantage in terms of costs. They do not charge upfront or admin fees; their APR ranges from 5% to 16%. Self charges a one-time $9 admin fee, and its APR is between 15.72% and 15.97%. This difference in fees and interest rates can potentially result in significant savings for customers who choose Cheese over Self.

- Timeline of Credit Reporting: Cheese is known for reporting payments to credit bureaus more quickly than Self, enabling customers to see improvements in their credit scores faster. This can be particularly important for individuals needing to boost their credit scores, such as those preparing to apply for a mortgage, auto loan, or rental agreement.

Customer Reviews and Ratings

To provide a well-rounded understanding of both services, we have summarized customer reviews and ratings3 from Trustpilot, BBB, Google Play, Apple Store, and other sources.

| Source | Cheese Credit Builder | Cheese Ratings | Self Credit Builder | Self Ratings |

|---|---|---|---|---|

| Trustpilot | 4.5/5 | 250 reviews | 1.6/5 | 51 reviews |

| BBB | N/A | N/A | 3.73/5 | 646 reviews |

| Google Play | 3.5/5 | 850+ reviews | 4.6/5 | 74.4K reviews |

| Apple Store | 4.6/5 | 1.7K | 4.9/5 | 234K reviews |

Customers of both Cheese and Self generally report positive experiences, praising the services for their ease of use, customer support, and effectiveness in building credit. Some users have noted that credit builder loans have helped them significantly improve their credit scores, enabling them to access better financial products and opportunities.

Cheese Credit Builder Reviews

Danny, Google Play: “I’ve been using Cheese for almost six months. I did not expect much out of it because online banking apps always seem shady. But honestly, I haven’t had any problems. The deposits come through on time, and the little bonuses have been lifesaving. I’m glad I switched!”

Mike, Google Play: “The Cheese app is easy to use and helps me keep track of my progress. I’ve been able to build my credit and save money simultaneously. Great customer support, too!”

Self Credit Builder Reviews

Jessica, Trustpilot: “Self Credit Builder has been a game-changer for me. I’ve been able to rebuild my credit after a tough financial period. The monthly payments are affordable, and it’s nice to see my credit score improving steadily.”

Kevin, Apple Store: “The Self app is user-friendly and informative. It has helped me manage my payments and monitor my credit score. I appreciate the transparency and simplicity of the service.”

Please note that these reviews are sourced from Trustpilot, Google Play, and Apple Store, and the content may change over time. The reviews provided here give a general overview of what real people say about Cheese Credit Builder and Self Credit Builder.

Comparison to Similar Offers

Chime Credit Builder

Chime Credit Builder is a secured credit card offered by Chime Bank. Unlike Cheese and Self, which are credit builder loans, Chime provides users with a credit card that requires a refundable security deposit. This deposit acts as the card’s credit limit, and the card can be used for everyday purchases. Payments made on the Chime Credit Builder card are reported to the major credit bureaus, helping to build your credit history. Chime does not charge annual fees or interest, making it a cost-effective option for building credit. However, it’s essential to remember that, unlike Cheese and Self, Chime does not help you save money simultaneously while building credit. (Relevant: Chime Review, Chime Debit Card, Chime vs Self, Chime vs Netspend, Chime Secured Card)

Kikoff Credit Account

Kikoff account offers a unique, no-fee credit-builder account that operates as a line of credit with a $500 limit. Unlike Cheese and Self’s credit builder loans, Kikoff allows users to spend up to their credit limit and only requires repayment of the amount used. Kikoff reports your payment history to the major credit bureaus, which contributes to your credit score. The advantage of Kikoff is that it does not charge interest or fees, and there are no hard credit inquiries when you apply. On the other hand, Kikoff does not have a savings component like Cheese and Self, meaning you won’t accumulate savings at the end of the term. (More: Kikoff Review, Kikoff Credit Account)

Credit Strong

Credit Strong is another credit builder loan service similar to Cheese and Self. It offers multiple loan terms and repayment plans, allowing users to choose the best option. Credit Strong reports your payment history to all three major credit bureaus, helping to establish your credit score. However, Credit Strong’s interest rates can be higher than Cheese’s, and it charges an upfront account activation fee. While Credit Strong does have a savings component, its costs, and interest rates might make it less cost-effective compared to Cheese or Self, depending on your financial situation and needs.

When choosing a credit builder service, it’s essential to weigh the pros and cons of each option carefully. Consider fees, interest rates, loan terms, and how the service reports your payment history. Analyze your unique financial situation and needs before deciding which service is right for you.

Conclusion

In conclusion, Cheese Credit Builder and Self Credit Builder are designed to help users establish and improve their credit scores. They share some core similarities, such as reporting payments to the three major credit bureaus and being FDIC-insured, which ensures safety and effectiveness in building credit.

However, there are notable differences between the two services that can impact your decision. Cheese stands out for its more flexible repayment plans, potentially lower costs, and faster credit reporting timelines. Cheese accommodates a broader range of financial situations with six different plans, whereas Self offers only four fixed 24-month plans. Additionally, Cheese does not charge any admin fees and provides lower APR options, depending on your state of residency, which may result in cost savings compared to Self’s one-time $9 admin fee and higher APR range.

Moreover, Cheese’s faster credit reporting timelines can help individuals improve their credit scores more quickly, which can be crucial for those who need a better credit standing for major financial decisions like applying for a mortgage, auto loan, or rental agreement.

Ultimately, the choice between Cheese and Self comes down to your unique financial situation and preferences. By carefully weighing each service’s features, benefits, and costs, you can decide which credit builder service best suits your needs. Whether you prioritize flexible repayment plans, lower costs, or faster credit building, selecting the option that aligns with your financial goals and circumstances is essential.

Frequently Asked Questions (FAQs)

Methodology

Our comparison of Cheese and Self is based on a thorough evaluation of their features, benefits, costs, customer reviews, and competitors. To analyze each service, we have considered factors such as loan terms, interest rates, fees, and credit reporting timelines. We aim to empower you with the information needed to decide which credit builder service best suits your needs.

Resources

Books

- “Your Score: An Insider’s Secrets to Understanding, Controlling, and Protecting Your Credit Score” by Anthony Davenport

- “The Total Money Makeover: Classic Edition: A Proven Plan for Financial Fitness” by Dave Ramsey

- “Rich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do Not!” by Robert T. Kiyosaki

- “Credit Secrets: 3 in 1. Boost Your FICO Score By 200 Points in Less Than 30 Days, Without Hiring Credit Repair Agencies.” by Neil Hack

Useful Sources

- Federal Trade Commission (FTC) – Building a Better Credit Report

- Consumer Financial Protection Bureau (CFPB) – Credit Reports and Scores

- National Foundation for Credit Counseling (NFCC)

- Experian – How to Build Credit

Disclaimers

- Interest calculated based on 12% APR

- The time it takes for a Cheese Credit Builder Account and payments to appear on a credit report varies. It depends on when the credit bureaus update your credit report.

- The ratings and review counts may change over time, so they should be verified with the respective sources before making any decisions. The information provided here is a general overview and comparison of customer ratings and reviews for Cheese Credit Builder and Self Credit Builder.